Becoming financially independent may sound like a nice theory. But the truth is that it is possible for anyone to achieve it. And I mean anyone, even someone who once had tens of thousands of student loan debts, like you and me. No matter what your financial problems are today, there is always a way to turn black again. Maybe trying a budgeting app is your first step.

In this article, I’m going to dive into the importance of financial independence and share some financial independence tips, including some that have worked for me.

What is financial independence?

Financial independence is about taking charge of your finances. You have a reliable cash flow that allows you to live the life you desire. You don’t have to worry about how to pay your bills or sudden expenses. And you’re not burdened with a bunch of debt.

It’s about realizing that you need more money to pay off debt, and maybe increase your income with a side hustle—we’ll get to that in a moment. It’s also about planning your financial situation for the long term by actively saving for emergencies or for retirement.

Table of Contents

How to become financially independent in 10 easy steps

Step# 1. Understand where you are

You cannot achieve financial independence without knowing your starting point. It can be discouraging to consider how much debt you have, how much money you need, and how much money you don’t have in savings. But this is a valuable step in the right direction.

Make a list of all of your debt: mortgage loans, student loans, car loans, credit cards, and any other debt you may have accumulated. Don’t forget to include any money you’ve borrowed from friends or family members over the years.

Now take a deep breath. And another one. Then add up all the numbers.

What are your debts?

If it’s a big number don’t freak out, I promise later in this article I’ll show you some ways you can pay for that. If it’s a small number, congratulations! Feel free to share your financial independence tips in the comments below.

Next, take a look at all the money you’ve saved.

Make a list of all your savings: savings accounts, stocks, company stock adjustment programs, company pension adjustment programs, and retirement plans. Then we add the recurring monthly payments you receive, such as Salary, money for part-time jobs, and so on.

Keep these numbers in mind as we work through the next few financial independence tips.

Step# 2. Look at money positively

Debt can definitely be a little daunting.

But remember that money is a good thing, even if it seems to be carrying a lot of weight right now.

You deserve to gain financial independence.

According to Sincero ‘s “You Are a Badass at Making Money”, people who don’t make a lot of money often feel embarrassed when it comes to making money. So the biggest obstacle that many people encounter when making money is that they feel like having money is bad. Many feel guilty for having it, and even more for wanting it. Sincero has said of money, “We use it every day to improve our lives, but we always seem to focus on the negative.”

Just like food and water, money is a basic necessity. It enables you to purchase the necessities and lead the lifestyle you desire.

To experience financial independence, you must view money as a tool to help you achieve your dreams, fuel you, and lead a stress-free life to enjoy.

Because when you see money negatively, you subconsciously sabotage your chances of making and keeping it.

Step# 3. Write down your goals

why do you need money?

Do you want to get rid of your debts for good? Are you dying to escape the 9-to-5 grind? Is there a place you’ve always wanted to travel to? Need to save for a wedding, kids, or retirement?

When I achieved financial independence, it was because I linked it to an emotional goal. My goal was to get out of student loan debt and start saving for my first home. And frankly, it was a euphoric experience to watch the debt shrink and my savings grow.

I was so excited when I saw the numbers change that I worked harder to make more money to see a bigger change in my personal finances. Would I have achieved my goal of financial independence if I hadn’t linked the goal to something emotional? Probably not. I was eager to leave my parents’ home and pay off my debt. This desperation has motivated me throughout my journey.

Another interesting thing happened. In February 2016, I wrote down some of my goals on a piece of paper:

- Earn $100,000 selling products online

- Save $20,000 on a down payment

- Pay off $24,000 in student loans

I ended up misplacing the paper and completely forgetting about it. And then, a little more than a year later, when I had moved into my new house, I discovered it in my notebook. In actuality, I had succeeded in all three. Funny thing was, I wasn’t even consciously considering those objectives.

You may not achieve everything you want to achieve in a month. But a year is a long time to make progress towards your goals. Make sure your goal is tied to a specific number you want to reach. Believe it or not, you will start working toward those goals without even realizing it.

Knowing exactly what you want to achieve makes achieving financial independence a million times easier.

Want To Learn The Exact Steps I Took To Become Financially Independent. Click Here To Find Out

Step# 4. Track your expenses

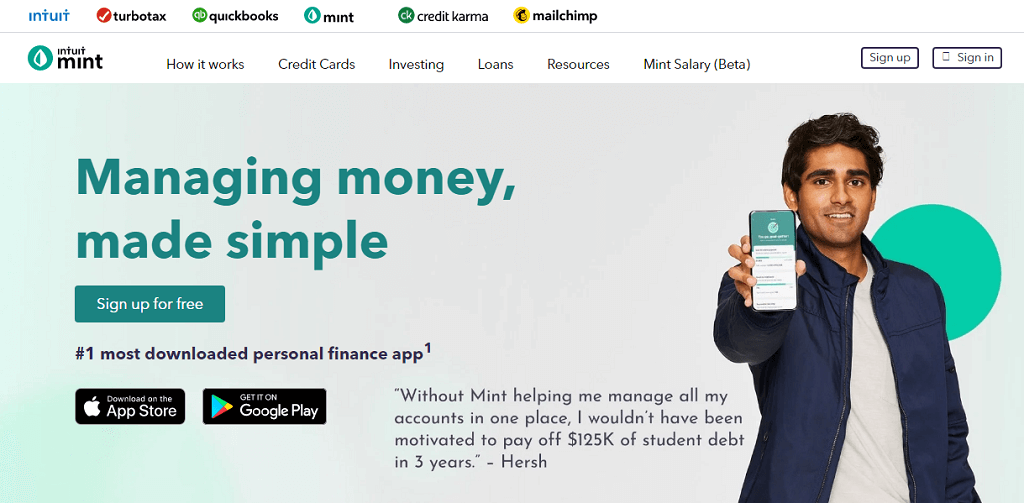

An important step towards financial independence is tracking your expenses.

You can use a tool like Mint that tells you how much money you’re spending, which categories you’ve overspent, how much money is in all your accounts, and how much you owe.

Another cool thing about Mint is that it lets you set goals within the dashboard. You can track your goals and know the exact month when you are expected to reach the goal based on how much money you have invested. So stay accountable and remind them to keep investing money for you.

After using Mint for a month, I managed to save some extra money for my new wedding fund goal. Mint has helped me focus on my goal and pushed me to create more passive income to meet my financial milestones.

Step# 5. Pay yourself first

You’ve probably heard the phrase “pay yourself first” before. However, if you haven’t done so, “pay for yourself first” means you put a certain amount of money into your savings account before you pay for anything else, e.g: Invoices. And the act of paying yourself first has helped countless people get one step closer to financial independence.

Why?

Because if you want to cash out $1,000 per billing cycle first, the rest has to go towards the bills. And if you don’t have enough to cover those bills, you need to earn an extra income to cover the expenses.

By paying yourself first, you guarantee that you will always have money set aside to invest in yourself. If you do the opposite, you only get what is left, which is usually not substantial enough to help you experience financial independence.

You can also pay yourself first in other ways. For example, if your company has a retirement plan, you can withdraw money for your retirement. In this way, you invest primarily in yourself and your future. The money is deducted from your salary, so all that’s left is money to set aside for your bills and expenses.

Step# 6. Spend less

Warren Buffett bought a five-bedroom house for $31,500 in 1958 and hasn’t moved since. His capital? A staggering $90.3 billion. He is able to purchase a larger, more expensive home. But he might be among the world’s wealthiest people due to his thrifty lifestyle.

Kanye West, on the other hand, isn’t afraid to flaunt his money. He lives in a $20 million mansion. And at one point, with $53 million in debt, he decided to ask Mark Zuckerberg for $1 billion… on Twitter.

The difference between the two super successful gentlemen? Buffett didn’t spend more than he needed to, and West is spending money he doesn’t have.

The truth is that a lot of rich people don’t look like rich people. Zuckerberg reportedly always dresses in the same boring t-shirt and jeans.

Buying less stuff can actually make you richer.

By spending less, two things work in your favor. First, you have more money to set aside for financial independence. Second, you’ll learn that you actually need a lot less stuff to survive, which also helps you put more money aside.

And that leads to our next point…

Step# 7. Buy experiences instead of things

Life is short. It’s not about hoarding all your money until you’re 65. You can enjoy life as long as you live.

Ultimately, the things that help you live a more fulfilling life will be your experiences, not the products you own.

And do the things you buy make you happier in the long run? Does the debt you have from buying a lot of stuff make your life easier?

Now let’s flip the switch.

What’s your happiest memory? What did you do? Who were you with?

Let’s just create more memories like this.

Maybe you have a friend that you like to train with. Invite them to a YouTube playlist at home for a free workout.

It’s date night. You want to make it unforgettable. Find a cool activity you’ve never done before at a fraction of the price on Groupon.

You’ve always dreamed of traveling to Rome. You saved money for a year to experience your dream vacation. Go on vacation without guilt. You didn’t go into debt for this, you earned it. Alternately, you may work remotely while traveling the world as a digital nomad.

Life is made up of moments. The best come from time spent with friends and family. While some products can help bring you closer to your family (like weekly family video game nights), most of them don’t offer much value.

Don’t spend money, you don’t have to pretend you have money.

Step# 8. Pay off your debt

Some people will tell you that investing your money in stocks is wiser than paying off your debt. If you’re an expert stock picker, maybe that’s true. But if you’ve never invested in stocks before, you could end up with more debt.

Many people feel the same way after paying off their last debt: relieved.

If you have $50,000 in debt, even if you have $30,000 in cash in the bank, you cannot truly call yourself financially free. You’re still $20,000 in the hole.

While paying someone else isn’t as glamorous as having money in the bank, it brings you closer to financial independence.

There are two main methods of paying off debt: snowball and avalanche. Snowball is when you pay off the smallest of debts first. When you pay off the debt with the highest interest rate, it is an avalanche.

You have to decide what works best for you. But as I worked to get out of debt, I had a snowball effect. It has helped me stay more motivated. Because I was able to pay off my first debt, a $1,200 credit card bill, in just a month, the sense of accomplishment helped motivate me to tackle a much larger, ongoing student loan.

And since credit cards were no longer a problem, I ended up paying about three times more than the meager $300 minimum payment on average. It ended up taking about three years to pay off the student loans instead of the nine years I was allotted.

Paying off a large debt takes an enormous burden off your shoulders. After paying off your debt, you will see the amount of money you have in the bank increase. It’s a great feeling to see the number go up (even if you had to watch it go down at first) and it keeps you motivated to keep increasing it.

Step# 9. Create additional sources of income

Now that we’ve established that, you’re undoubtedly asking yourself, “How can I pay off my debt if my income is insufficient?”

If you’re serious about financial independence, you’ll have to sacrifice some blood, sweat, and tears.

Your 9 to 5 may not cut it. If that’s the case, you need to step it up and look for money outside of your current job.

Some experts recommend having seven streams of income. If you’ve got a 9-to-5 job, congratulations, you’ve got one, just six more!

Now you can look at your sources of income in two ways: active income (trading time for money) or passive income (money that can come in while you sleep).

If you’re trading your time for money, you’re limited by the hours of the day. Here are a few side jobs you can do to earn an active income:

- Become a freelance writer by finding jobs on

- Help a business owner with jobs on Upwork as a virtual assistant

- Gain new skills through online courses for entrepreneurs and make money

- Become an Uber driver

- Help with household chores on Task Rabbit

- Take a job or two on Craigslist

- And more!

If you don’t have much time to devote to earning income, you can focus on increasing your income streams with passive income, such as:

- Starting a dropshipping online store

- Start your own print-on-demand store

- Sell profitable content (blog, e-books, courses, webinars, audiobooks, podcasts, apps)

- Become an affiliate marketer

- Buy and rent real estate

Fortunately, all seven of your sources of income can originate from the same place. For example, if you’re an eCommerce pro, your income streams might come from building seven different stores. And remember: you don’t have to start with seven streams, you can build up over time.

Step# 10. Invest in your future

The last tip on financial independence is an important one. Suppose you follow the advice and recommendations in this article, become debt-free, and increase your savings. That might be enough to help you now. But what if the unexpected happens? Will you be ready for this?

It’s important to have money set aside for rainy days, retirement, and (sorry for being morbid here) in case you die to make sure your family doesn’t drown to cover your funeral, debts, and taxes paid. Okay, now let’s get back to that happy place.

If you have that 9-to-5 job, talk to your company about adding a retirement plan or see if you’re already getting deductions for it. The deduction is made before it is credited to your account, so you never feel like you are losing any money. And it’s pretty cool to check back regularly and see your savings grow.

Next, you should set aside money for an emergency fund. According to some experts, $10,000 is acceptable or six months of your salary. And to be honest, these numbers can seem pretty high if you’re not making a lot of money. Instead, start with a goal you can afford — like $100 the first month. And as you start earning more active or passive income, increase your goal to $500 a month to $500 every two weeks, and so on. If you’ve overspent and have a big credit card bill due, don’t use your emergency fund — focus on pursuing more active income opportunities so you can pay it back faster.

The emergency fund is only for unplanned emergencies like a tree falling on your house, a car accident that you have to pay for out of pocket, or a hospital visit.

By setting aside money for rainy days and retirement, you’re less likely to end up back where you are now: the desire for financial independence.

Want To Learn The Exact Steps I Took To Become Financially Independent. Click Here To Find Out

Conclusion

Financial independence can help you take control of your finances and, more importantly, your life. It’s about living within your means, being a little frugal, and making sure the money is spent on things you really need, like food, shelter, and yes even vacations (relaxation is important, too, you know). By following the financial independence tips in this article, you can get one step closer to the financial independence you deserve. So take a look at those finances, build additional income streams, pay off those debts, and before you know it, you’ll be free.